Monthly Highlights

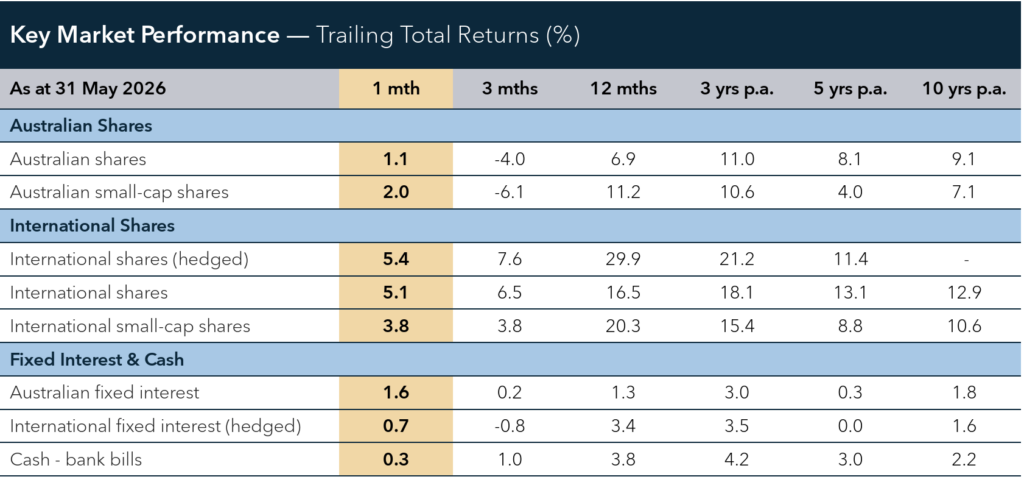

Global share markets continued to advance in May, supported by resilient corporate earnings, improving confidence in the global growth outlook and ongoing investment in artificial intelligence related infrastructure. While geopolitical risks and inflation concerns remained in focus, easing energy prices and stronger investor sentiment helped support gains across major markets. Bond markets also stabilised later in the month as yields eased from elevated levels.

Australian shares delivered positive returns but continued to lag major offshore markets. Gains were led by materials, as copper prices surged on expectations of stronger demand from AI infrastructure and electrification trends. Healthcare and energy were among the weaker sectors, with healthcare pressured by sector-specific earnings concerns and energy giving back some of its earlier strength as oil prices eased. Smaller companies outperformed larger peers as participation broadened across the market.

International shares produced another strong month of returns across both developed and emerging markets. The US remained a key driver of performance, supported by technology and growth companies, while Europe and Japan also posted solid gains. Emerging markets outperformed, led by strength in Korea and Taiwan, where companies linked to semiconductor production and AI supply chains continued to benefit from strong investor demand.

Australian and global fixed interest markets delivered positive returns in May as bond yields eased from their intra-month highs. Australian bonds outperformed following softer inflation and labour market data, prompting investors to scale back expectations for further interest rate increases following the RBA’s recent tightening cycle. Credit markets remained resilient, supported by healthy corporate fundamentals, although inflation and geopolitical risks continued to temper sentiment.

Market observations

Markets continue to grapple with the conflict in the Middle East, as uncertainty fuels elevated volatility across asset classes. A prolonged disruption to oil supply could undermine growth and reignite inflation pressures. But the broader structural outlook remains constructive. Recent market moves reflect the run of economic data, earnings announcements and optimism that the conflict in the Middle East will soon end.

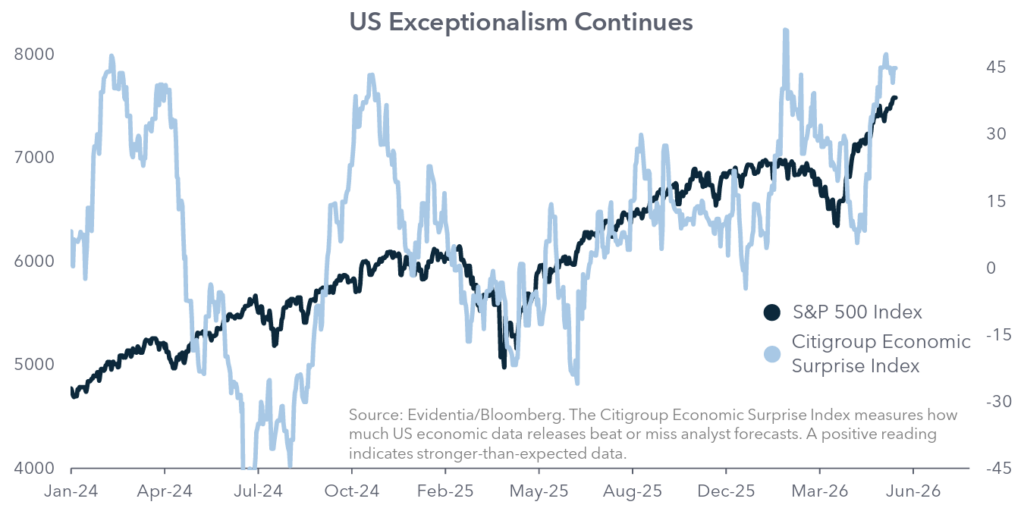

The US economy continues to lead the pack. Corporate earnings have been exceptionally strong, with 84% of S&P 500 companies beating expectations. The AI investment boom remains a powerful engine of growth, driving impressive results across technology, communications and related sectors. Meanwhile, the American consumer has proved remarkably resilient, supported by a healthy labour market, rising wages and ongoing fiscal stimulus. Together, these forces have propelled US equities to fresh record highs. Inflation, however, remains a watch point, with price pressures still running above the Federal Reserve’s target and bond markets becoming increasingly sensitive to the prospect of tighter policy. Even so, the prevailing outlook remains one of solid growth and supportive conditions for risk assets.

Australia’s story is more nuanced. Inflation remains uncomfortably high and the RBA’s three rate increases this year are beginning to bite, cooling domestic demand and weighing on household budgets. Consumer-facing businesses and financial stocks have struggled, while resource companies have benefited from a lift in commodity prices. Economic growth is expected to remain below trend as restrictive monetary policy works its way through the system. Although further tightening remains possible, markets currently anticipate only one additional rate increase.

The 2026 Federal Budget added another twist to the domestic outlook, introducing changes to negative gearing and capital gains tax. These measures are expected to temper housing demand, slow credit growth and place pressure on bank earnings. However, their long-term impact on broader equity valuations is likely to be limited, as global capital and superannuation flows help absorb shifts in domestic investor behaviour.