Our highlights

Global markets made a positive start to the year despite a heavy flow of headlines. Renewed tariff threats, geopolitical risks, a weaker US dollar and bond market volatility created a noisy backdrop, but investors remained focused on resilient economic conditions and earnings growth. Fiscal and inflation concerns weighed on government bond markets, while volatility picked up again in early February following a pullback in technology companies as AI-related valuations were reassessed.

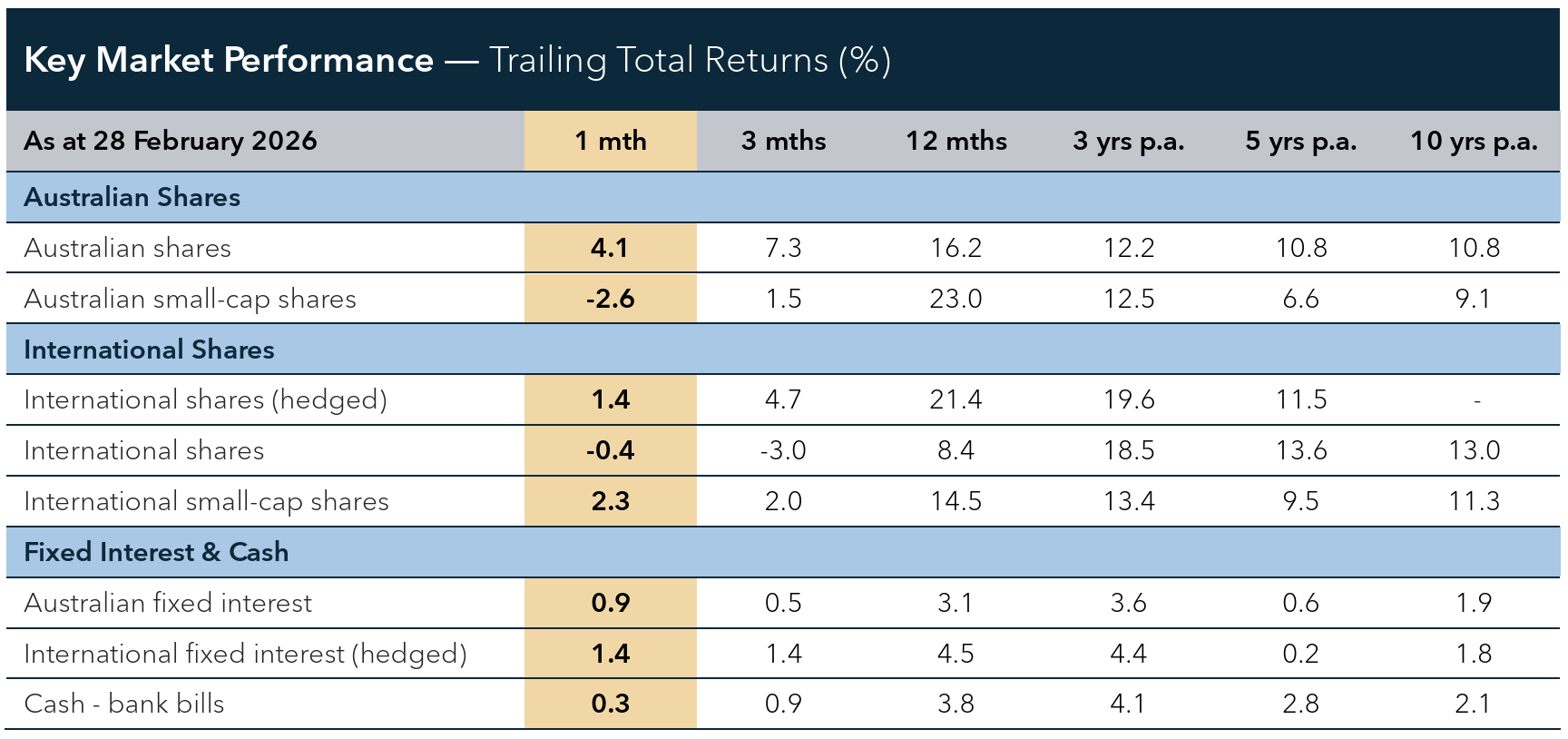

Australian shares moved higher, led by financials and materials, as the reporting season highlighted resilient bank earnings and improving conditions across the mining sector. Consumer staples and utilities also performed well given their defensive earnings profiles, while healthcare and IT lagged following weaker reporting-season reactions and pressure on growth valuations. Consumer discretionary also declined as cost-of-living pressures weighed on household spending.

International shares were mixed in February. The US market declined as technology shares fell amid ongoing concerns about AI-related disruption. European markets rose as investors favoured relatively cheaper markets outside the US, while Japan gained after the incumbent government secured a landslide election victory. Chinese markets fell amid ongoing concerns about the property sector. Global listed property and infrastructure also performed well as bond yields declined.

Global fixed interest markets edged higher as government bond yields drifted lower. Softer US ination data and more measured central bank commentary supported government bond prices, while returns from corporate bonds were modest as credit spreads widened modestly, indicating investors demanded more compensation relative to government bonds to hold credit risk.

Market observations

Australian half-year reporting season

The half-year reporting season showed the economy remains resilient, supported by lower interest rates and stronger commodity prices. Earnings expectations improved, led by financials and resources, while healthcare and consumer discretionary were weaker.

Artificial intelligence (AI) was a major theme, contributing to a broad sell-off in technology and media shares as investors reassessed how AI could disrupt traditional software and digital business models.

Overall, earnings growth is recovering after several softer years and is beginning to broaden beyond the resources sector, supporting a more balanced outlook for the ASX.

Middle East conflict and global markets

The recent escalation in tensions involving the US, Israel and Iran has introduced a new source of uncertainty for global markets. While the situation remains fluid, investor attention has focused primarily on the potential impact on global energy supply.

A key concern is the Strait of Hormuz, a narrow shipping corridor in the Middle East through which a signifcant share of the world’s oil exports pass each day. Disruption to shipping through this route has raised concerns about the reliability of global energy supply and pushed oil prices higher.

Energy markets are the main channel through which geopolitical events such as this affect the broader economy. Higher oil prices can feed through to transportation costs, manufacturing and food production, potentially placing upward pressure on inflation and slowing economic growth if sustained for an extended period.

Importantly, markets are also assessing whether the current disruption is likely to be temporary or more prolonged. Oil prices often react quickly to geopolitical shocks, but longer-term economic consequences typically depend on how long supply issues persist.

History provides some perspective. Financial markets have experienced numerous geopolitical events in the past several decades, from conflicts in the Middle East to the invasion of Ukraine. While these events can cause short-term volatility, they have generally had limited long-term impact on investment returns unless they fundamentally change global economic conditions.

For investors, the key variables to watch in the coming weeks will be developments in the conflict itself, the extent of any disruption to energy supply, and the trajectory of oil prices. As always, maintaining a longterm perspective remains important during periods of heightened uncertainty.