Introduction

Market volatility is an investment term used to describe when a market experiences a period of unpredictable and sharp price fluctuations. People often think about volatility only when prices fall. However, volatility can refer to sudden price rises, too. For this Insight, we will focus on volatility in terms of share market downturns, as this tends to worry investors the most.

While company and sector-specific performance can cause volatility in the share prices of individual companies, short-term volatility experienced across the broader market is typically driven by sentiment surrounding macroeconomic and geopolitical factors. In the current environment, there are several of these factors at play that are combining to unnerve and cause volatility in markets — stubborn inflation, expectations of higher-for-longer interest rates, slowing economic growth, the ongoing war in Ukraine, a weaker-than-expected Chinese recovery, and more recently, conflict in the Middle East.

Yes, market volatility is unsettling. Nobody likes seeing negative returns or the value of their investments fall, even if history tells us those falls are only temporary. However, it is essential to understand market volatility is a normal part of investing. Eliminating market volatility is not possible without removing risk, and risk is the price investors pay for higher returns over the long-term.

A better approach is to accept and prepare for periods of market volatility. By being prepared, investors are far less likely to be alarmed and make poor decisions when markets become volatile. Instead of worrying about market volatility, a much better use of time is to focus on their long-term investment strategy, goals and objectives. In this Insight, we cover some key concepts to help investors better navigate market volatility.

Turn down the noise

In investing, noise refers to anything that distracts us from making sound, long-term decisions. Markets are flooded daily with headlines, commentary, and data — much of it focused on predicting short-term movements. The mainstream media often amplifies this noise by highlighting the negatives because, as the old saying goes, “bad news sells.”

Learning to tune out the noise is especially important during periods of heightened market volatility. It allows us to stay grounded, avoid emotional reactions, and focus instead on making thoughtful decisions based on long-term fundamentals. Most of what dominates the headlines today is unlikely to be as relevant five or ten years from now.

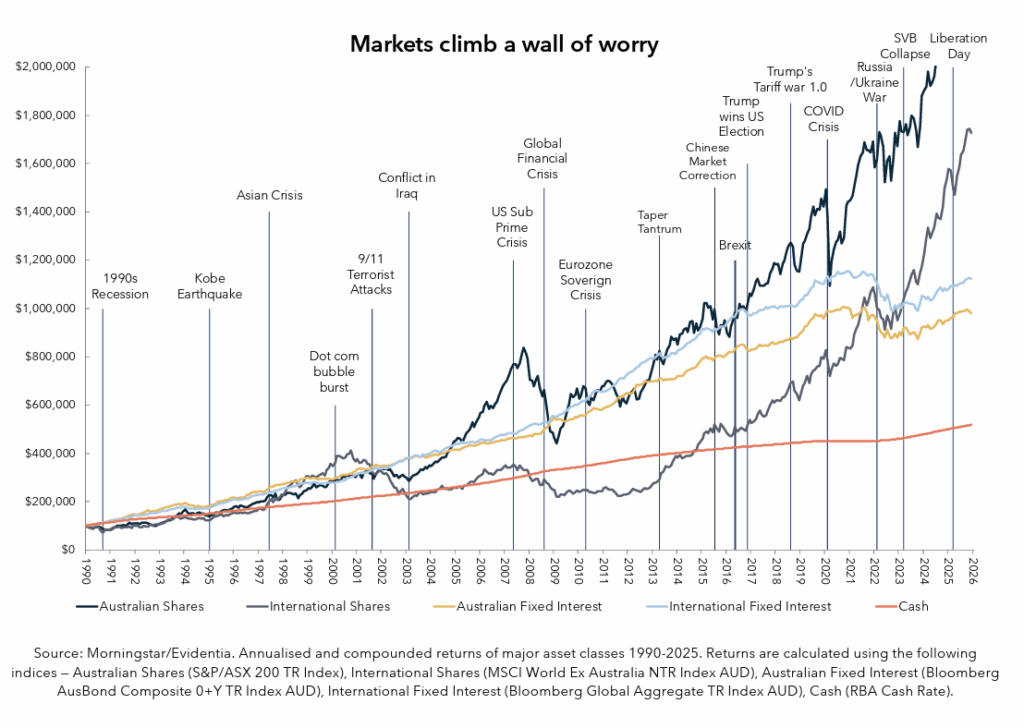

History offers valuable perspective. The chart below shows how major markets have performed since 1990 — through recessions, political upheavals, natural disasters, and global crises. Despite these events, markets have continued to rise over the long term, climbing what’s often called the “wall of worry.” This reminds us that while short-term noise can be unsettling, staying focused on long-term goals has consistently been rewarded.

Think like an investor

One of the benefits of taking a long-term approach to investing is that time is on an investor’s side. While speculators focus on short-term market sentiment and price movements, disciplined and patient investors focus on the long term, understanding that investing is a marathon, not a sprint. Investors are able to ride out short-term market volatility and stick to their long-term strategy, knowing fundamentals will push the market higher over time. But why do share markets trend upwards?

At its core, investing in share markets is about investing in and becoming a part-owner of some of the world’s largest and highest-quality companies across a wide range of industries. These companies produce essential products and services that we use in our day-to-day lives. Many are household names — companies like Apple, Microsoft, Amazon, Tesla, Samsung, BP, Nestle, Coca-Cola, Commonwealth Bank, BHP Group, Origin Energy, CSL and Telstra to name only a few.

Over time, economies tend to grow as populations increase and improvements are made in productivity through innovation. As economies expand, companies’ earnings also grow. Company earnings are then either reinvested back into the company to increase future earnings, or are paid out as dividends to investors who will either reinvest or spend the dividends on products or services. Either way, company earnings growth is what ultimately drives share prices higher, increasing the value of those companies. Collectively, as companies become more valuable over time, so does the broader share market.

Although market sentiment can change daily due to the endless flow of positive and negative news and events and cause share prices to fluctuate higher or lower, little of this is relevant to the underlying companies. As long as the fundamentals of these high-quality companies remain intact and they continue to grow earnings, it is only a matter of time before the sentiment turns in their favour. Thinking like an investor or a part-owner of some of the world’s best companies can be an effective way of ignoring the noise in the short term and instead focusing on the long term.

History shows that betting against the market rarely pays off. Since its inception, the S&P 500 Index — a widely used benchmark for US shares — has delivered annualised returns of approximately 10% per annum, recording positive returns in nearly three out of every four years. The long-term performance of Australian shares has been even more favourable for investors. As illustrated in the chart below, the S&P/ASX All Ordinaries TR Index shows that Australian shares have returned approximately 13% per annum since 1900, with negative calendar year returns occurring only about once every five years.

![]()

Time in the market, not timing the market

Markets tend to rise over the long term but often experience short-term volatility, with declines typically occurring faster than gains. This volatility can challenge even seasoned investors. Some attempt to navigate this by timing their entry and exit, trying to avoid downturns and capture upswings — known as ‘market timing.’ However, predicting short-term market movements is nearly impossible, making this approach highly risky.

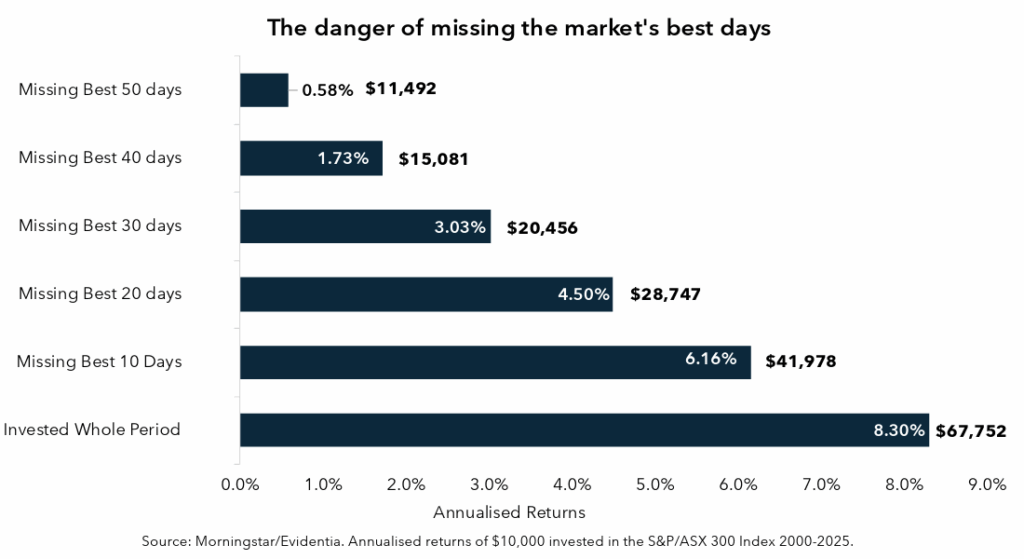

The biggest risk of market timing is being uninvested when markets unexpectedly rebound. Moving out of growth assets like shares into defensive ones like cash during these moments can result in missing the market’s best days, significantly impacting long-term returns. The chart below illustrates the annualised returns of Australian shares and a hypothetical $10,000 investment in 2000, comparing the outcomes of remaining fully invested versus missing some of the best return days.

If an investor had remained invested in Australian shares over this period, their $10,000 would have grown at an average annual rate of 8.30%, reaching $67,752. However, if they had tried to time the market and missed just the 20 best days, their investment would have grown to only $28,747 — less than half. Missing the best 50 days would have caused their initial $10,000 investment to lose value after accounting for inflation.

Importantly, many of the market’s strongest daily gains tend to occur during periods of heightened volatility, often close to major market declines. This clustering of best and worst days is precisely what makes stepping out during periods of uncertainty so risky, as most investors are unlikely to avoid the worst days while still being invested for the subsequent rebound. The key to successful long-term investing is maintaining the discipline and patience to stay invested. Time in the market, not timing the market, builds wealth.

Market declines are common but they never last

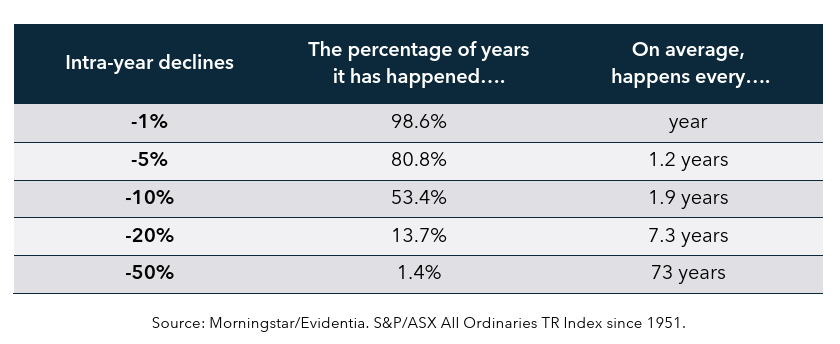

Market declines are more common than most people might think. The table below shows how frequent intrayear declines have been in the Australian share market over the past 74 years. On only one occasion during this period did the market avoid a negative daily move of more than -1% (1959). Pullbacks of 5% are very common, occurring on average every 1.2 years. ‘Market corrections’ — defined as a fall in an index of greater than 10% but less than 20% — have happened in just over half of the years and, on average, are expected to occur every two years. While investors should, on average, expect to experience a ‘bear market’ in Australian shares — a fall in an index of 20% or greater — every 7.3 years.

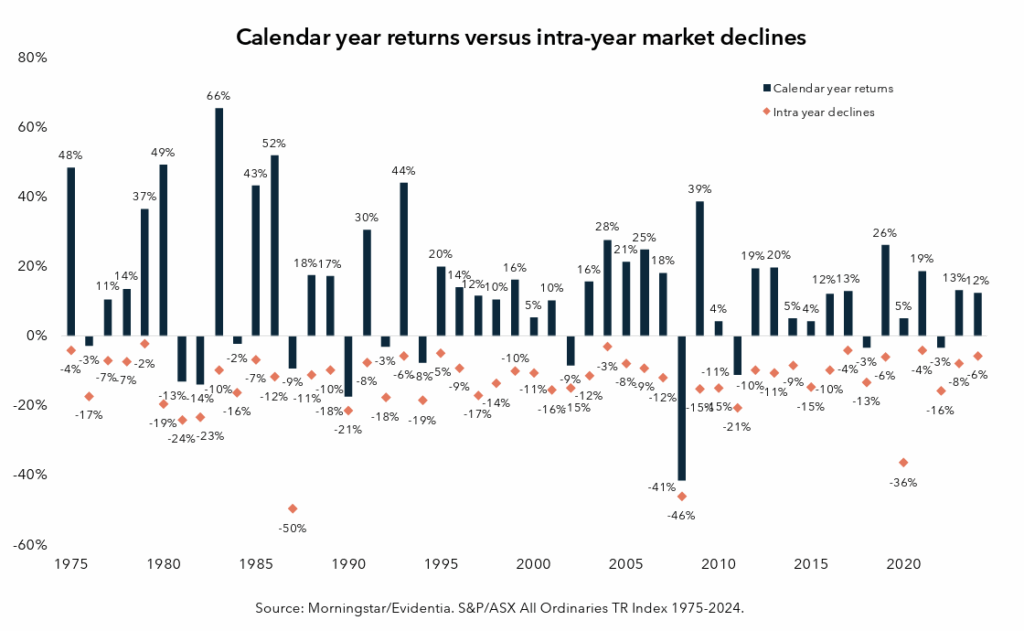

The chart below compares calendar year returns and the largest intra-year declines in the Australian share market over the past 50 years. Although the end-of-calendar-year returns have been overwhelmingly positive, it is rare that the market will go through an entire year without experiencing a meaningful decline at some stage. While unsettling, short-term market volatility is inevitable and a normal part of investing. Disciplined, patient, and long-term focused investors understand this and know that, over time, markets always recover and go on to post gains.

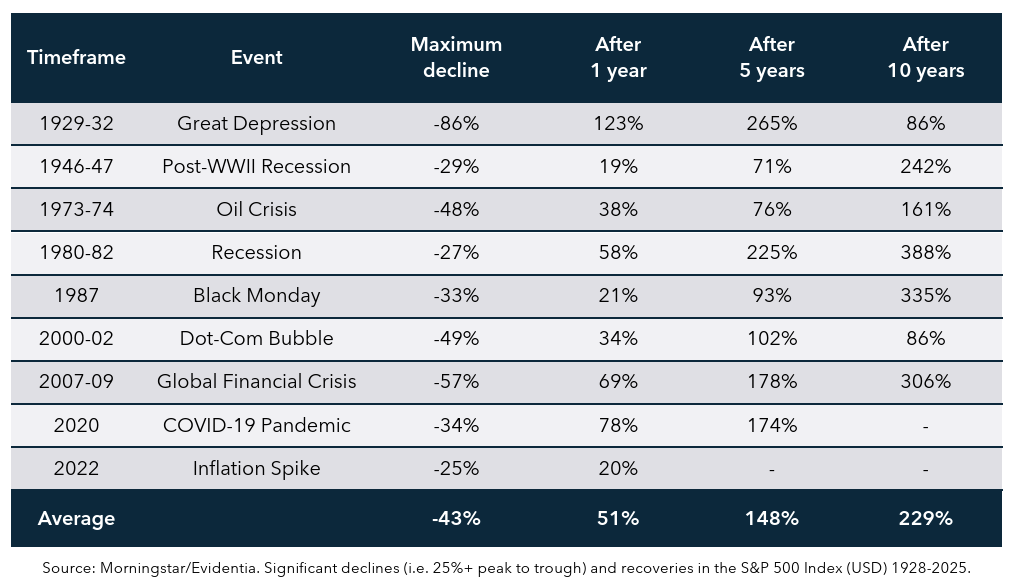

Major market downturns bring opportunities

Historically, major market downturns have presented excellent opportunities to invest in shares as markets have rebounded and gone on to post strong long-term gains. The table below shows key historical events that have triggered significant declines of 25% or greater in US shares, along with the cumulative returns following the end of those declines. One year after a 25%+ decline in the market, investors experienced an average gain of 51%. Five years later, the market was 148% higher. Ten years after a significant fall, the average gain was over 200%, which equates to an annualised return of approximately 12% per annum. This compares favourably with the long-run average return on US shares of 10% per annum.

Shares invariably bottom and recover quickly when markets are most negative because investors often overreact, pushing prices to levels well below their fundamental valuations. Those who sell during a market downturn effectively transfer wealth to those who buy and stay the course.

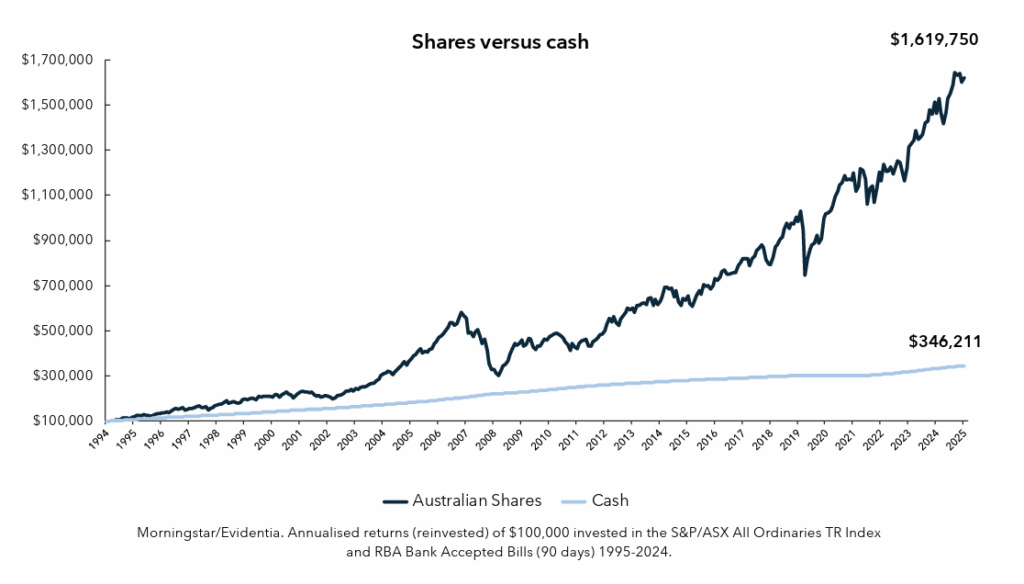

The hidden cost of cash

A common reaction of investors to periods of heightened market volatility is to switch out of growth assets like shares and into defensive assets like cash. With interest rates higher than they have been in over a decade, the temptation can be even greater. While the safety promised by cash can be alluring, the sense of safety can be a false one. A hidden cost of investing only in low-risk defensive assets is the upside forgone by not investing in growth assets like shares. For investors still accumulating wealth for retirement, this means their savings are not working for them and, ultimately, a smaller nest egg. For investors in retirement, relying solely on cash can increase the risk of running out of savings later in retirement.

Over the longer term, returns from growth assets have been higher than those from defensive assets. These higher returns are important, as they help to mitigate the effects of inflation and maintain the purchasing power of an investor’s capital and income. The income-only returns from cash, on the other hand, rarely outpace inflation by any meaningful margin over time. A higher allocation to growth assets typically means a high allocation to shares. In addition to providing capital growth (share price appreciation) over the long term, most shares yield a regular, growing income in the form of dividends. Australian shares, in particular, have traditionally been generous dividend payers (many of them with the added bonus of attached franking credits) relative to shares listed in other countries. The chart below compares the performance of an initial $100,000 investment in cash and in Australian shares. Despite much higher short-term volatility, the longterm returns from shares far outweigh those of cash.

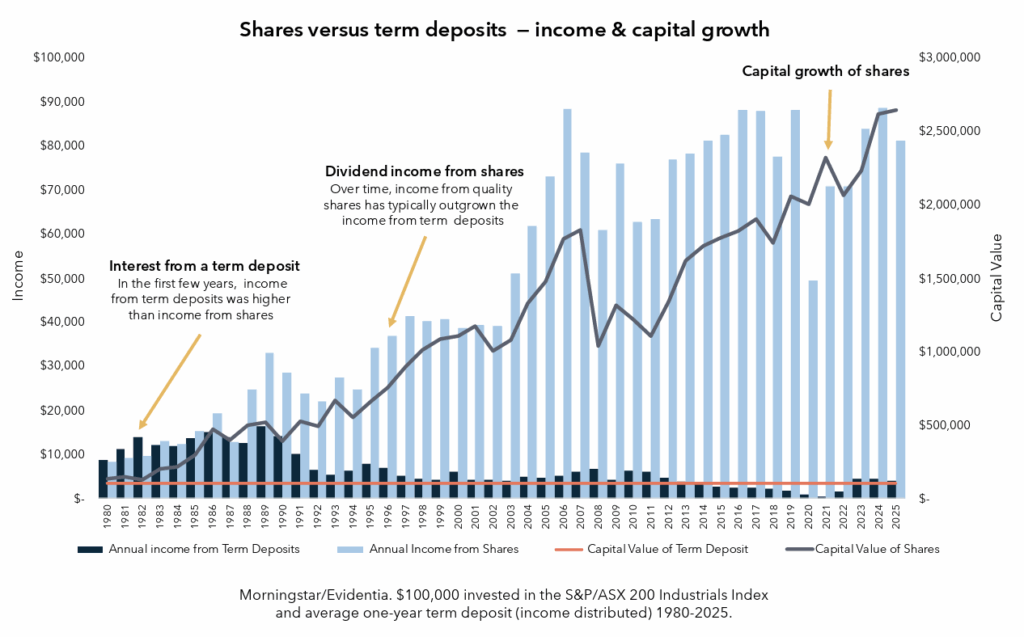

Term deposits are also a popular choice among investors. While they generally offer higher interest rates than cash, their long-term returns fall well short of the total returns — combining both income and capital growth — delivered by shares. Moreover, unlike cash, which can be accessed at any time, term deposits are locked in for a fixed period, potentially limiting an investor’s ability to respond to emerging investment opportunities.

The chart below compares the long-term returns of Australian shares with the average returns from one-year term deposits. It tracks the performance of an initial $100,000 investment, assuming all income is distributed rather than reinvested. A key takeaway is that, while income from term deposits initially exceeded share dividends during the high-interest-rate environment of the early years, dividend growth has since far outpaced term deposit income. Furthermore, while $100,000 invested in a term deposit in 1980 would still be worth only $100,000 by the end of 2025, the capital value of the shares has grown to more than $2.5 million — easily outstripping inflation.

Diversification

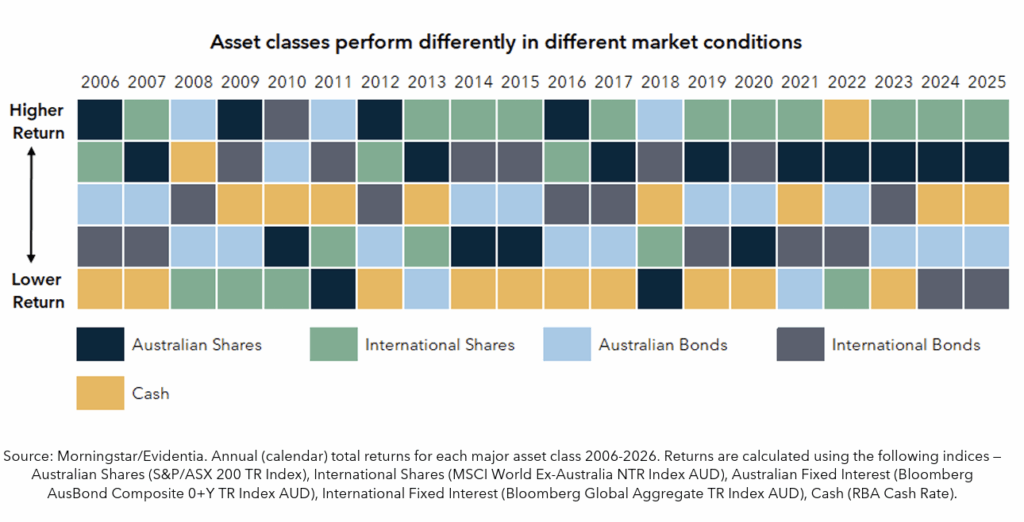

While media headlines about markets tend to focus on specific indices like the S&P 500 or the S&P/ASX 200, the reality is that most investors hold a much broader spread of assets in their portfolios. Diversification is an important investment strategy because it helps reduce risk and produce more consistent returns across market conditions, particularly when markets are volatile. It does this by spreading an investor’s portfolio across and within a range of asset classes, such as shares, bonds (fixed interest), and cash — a process called ‘asset allocation’ — which tend to perform differently from one another at different times in the market cycle. There is no set standard for how and where to allocate across a portfolio. Instead, this is tailored to each investor’s circumstances, goals, objectives, and risk tolerance.

The table below shows the past 20 years of annual returns for some major asset classes commonly held in Australian investor portfolios. What stands out is how differently the asset classes perform and how difficult it is to predict which will perform best in any given year. Rather than chasing top-performing asset classes, a more sensible approach is to diversify a portfolio across a range of asset classes that will perform better collectively in all market conditions.

Investing through volatility

For many investors, investing is an ongoing process rather than a one-off decision. Regular contributions to superannuation or regular investment plans mean money is invested consistently over time, regardless of short-term market movements — an approach known as dollar-cost averaging.

While market volatility can feel uncomfortable, it can work in favour of investors who are still accumulating assets. When markets fall, regular contributions buy more units at lower prices, and when markets rise, fewer units are purchased at higher prices. Over time, this can result in a lower average purchase price and a greater number of units once markets recover.

Dollar-cost averaging also delivers a powerful behavioural benefit. By spreading investment decisions over time, it reduces the pressure to “get the timing right” and lowers the regret associated with investing just before a market downturn. Rather than trying to predict short-term market movements, investors can focus on consistency and discipline. In this way, regular investing helps turn market volatility from a source of anxiety into a long-term advantage.

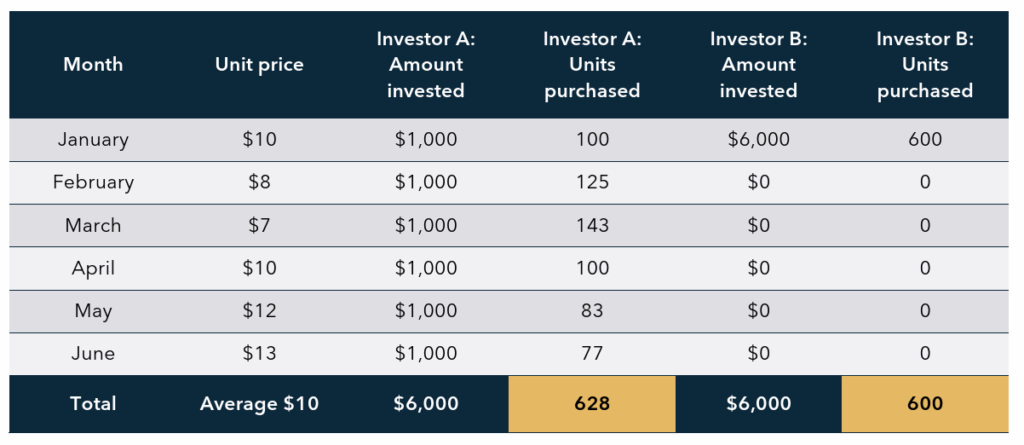

The table below illustrates this concept by comparing two investors who each invest $6,000 over six months using different approaches. Investor A invests $1,000 each month, while Investor B invests the full amount upfront. As shown, Investor A accumulates 628 units (average unit price of $9.55) compared with Investor B’s 600 units (average unit price of $10.00), despite both investing the same total amount. This example highlights how dollar-cost averaging can help smooth the impact of market volatility, reduce the risk of poor timing, and potentially enhance long-term outcomes.

It is important to note that dollar-cost averaging is not always the most effective strategy from a purely returnfocused perspective. Vanguard research shows that in generally rising markets, investing a lump sum upfront has historically delivered better outcomes about two-thirds of the time because it is invested sooner. However, dollar-cost averaging can be valuable during volatile markets, after extended rallies, or for more risk-averse investors. In these situations, it can help manage behavioural risks and support investment discipline, particularly compared with remaining in cash.